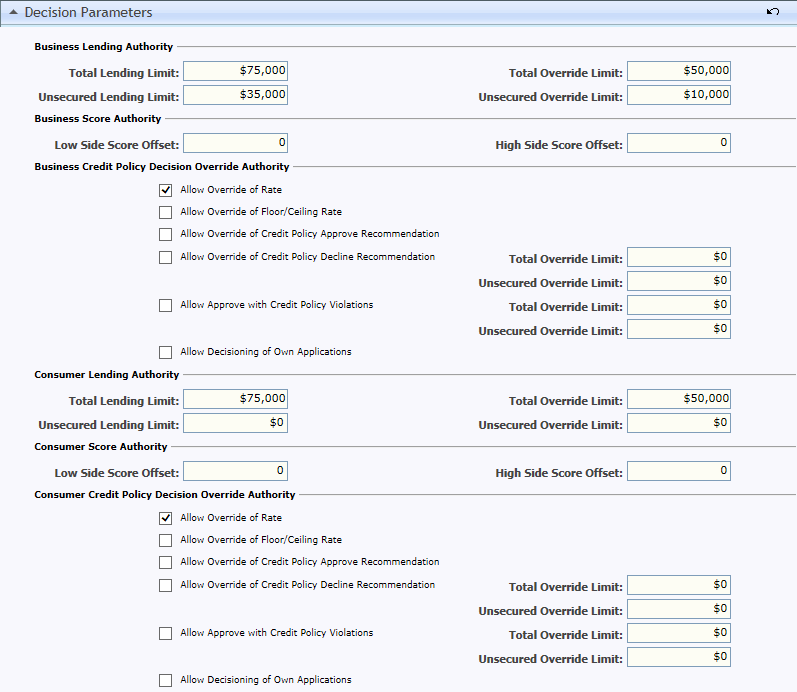

Lending authority is defined as lending limits for the total existing bank exposure for the relationship. The total existing bank exposure for the relationship is defined as the sum of the current outstanding loan balance plus the sum of all requested amount(s) for all approved product(s) on the application. Your Baker Hill Origination Administrator must define an Underwriter’s lending limits (as part of the Underwriter’s security record) before that Underwriter will be able to approve applications.

If an Underwriter has insufficient lending authority to approve an application, the Underwriter can send the application to another Underwriter for co-decisioning. If your financial institution is using additive lending authority, the lending limits of the co-decisioners will be added together; as long as that total exceeds the total existing bank exposure, the application can be approved. If your financial institution is using non-additive lending authority, the final Underwriter must be able to approve the entire requested loan amount on his or her lending authority alone.

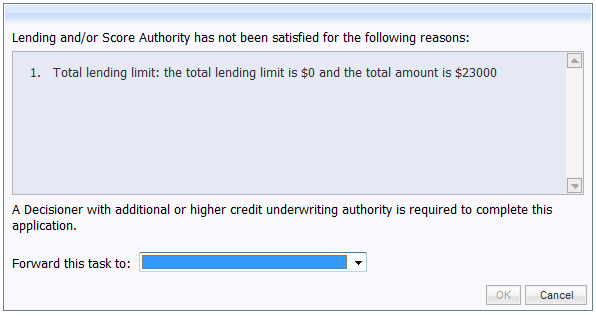

Origination will not allow users without the proper authority to approve or counteroffer applications; in these cases the application must be forwarded to another user with the proper authority in order to complete the decisioning process. The figure below shows the message that is displayed if a user without the proper authority attempts to approve or counteroffer an application:

Score Authority determines (based on application score) whether a user can override a recommended decision. This feature closely resembles the Score Authority functionality in Fair Isaac’s SBSS Credit Desk. Score authority is defined in terms of a number of points above and below the financial institution’s evaluation cutoff score. In Baker Hill Bank2Business, score authority does not apply in applications that do not have principal/guarantor entries or that are returned for any other Scoring Exception (in both cases, only a non-predictive score is returned, making scoring authority inapplicable).

Please note that if your institution utilizes more than one offering in Baker Hill Origination, lending authority and score authority are set up separately. If you have access rights to both, your limits may be different for each.

Lending Authority

Your financial institution can select one of two options regarding how lending limits are set:

Use separate lending limits for total and unsecured transactions (split lending authority).

Use a single-limit lending option. In this case, you won’t see the options relating to secured/unsecured limits mentioned in this documentation.

Whether you’re using the split or single-limit lending option is defined in your initial setup by your financial institution.

Note for Bank2Business applications: Optional fields in the General Business Information section of the Bank2Business application are available for the Relationship Manager to enter the customer’s current exposure. If you’re using total/unsecured limits, you’ll see a Total Existing Secured Exposure field and a Total Existing Unsecured Exposure field. These two fields will be added together to determine the total current exposure. If you’re using a single total lending limit, you’ll see just one field: Total Existing Bank Exposure.

Note for Baker Hill Bank2Consumer applications: Even if your institution is configured for the split lending option, only the Total Existing Bank Exposure field is present. The Bank2Consumer Application page doesn't differentiate between total and unsecured exposure, though the total takes into account all exposure, both secured and unsecured.

Note for Baker Hill Bank2Dealer applications: Because only the single-limit lending authority option is available in Bank2Dealer, total and unsecured lending does not apply to the Bank2Dealer solution.

Note for all Baker Hill applications: If the exposure fields are not completed for an application, the decisioning form will include a standard credit policy information message stating that the total existing bank exposure was not provided.

Note for all Baker Hill applications: A decisioning parameter checkbox in the Lending Parameter section for each offering allows Administrators to indicate if a user can decision (Approve, Counteroffer) an application which they had created. If your institution does not allow this activity, deselect this checkbox to force the user to forward the application to another user for decisioning. This only applies to Approve and Counteroffer decisions.

Total and Unsecured (Split) Lending Authority

If your institution is using the split lending authority option, the unsecured lending authority is considered a subset of the overall total. Note: You enter a separate amount as the unsecured limit.

As long as the unsecured loan request is equal to or less than the unsecured lending authority, and as long as the total amount of the loan request (unsecured + secured) is equal to or less than the Underwriter’s total lending authority, he/she has the authority to approve the request.

Please see the following figure and examples for further explanation:

• Example 1 • |

|

Underwriter’s Total Lending Authority |

$75,000 |

Underwriter’s Unsecured Lending Authority |

$35,000 |

Amount Requested and Approved (Secured) |

$50,000 |

Amount Requested and Approved (Unsecured) |

$0 |

Existing Exposure (Secured) |

$15,000 |

Existing Exposure (Unsecured) |

$10,000 |

Conclusion: Two conditions must be met in order for the Underwriter to have the authority to approve the request:

$50,000 + $0 + $15,000 + $10,000 = $75,000 The total of request + exposure is equal to or less than the total lending authority of $75,000, so this condition is met.

$0 + $10,000 = $10,000 The total of unsecured request + exposure is equal to or less than the unsecured lending authority of $35,000, so both conditions are met. |

|

• Example 2 • |

|

Underwriter’s Total Lending Authority |

$75,000 |

Underwriter’s Unsecured Lending Authority |

$35,000 |

Amount Requested and Approved (Secured) |

$50,000 |

Amount Requested and Approved (Unsecured) |

$10,000 |

Existing Exposure (Secured) |

$15,000 |

Existing Exposure (Unsecured) |

$10,000 |

Conclusion: $50,000 + $10,000 + $15,000 + $10,000 = $85,000

$10,000 + $10,000 = $20,000

|

|

• Example 3 • |

|

Underwriter’s Total Lending Authority |

$75,000 |

Underwriter’s Unsecured Lending Authority |

$35,000 |

Amount Requested and Approved (Secured) |

$20,000 |

Amount Requested and Approved (Unsecured) |

$30,000 |

Existing Exposure (Secured) |

$15,000 |

Existing Exposure (Unsecured) |

$10,000 |

Conclusion: $20,000 + $30,000 + $15,000 + $10,000 = $75,000

$30,000 + $10,000 = $40,000

|

|

Single-Limit Lending Authority

If your institution is configured to use the single-limit lending authority option, you simply have a total lending authority amount. As long as the loan request amount is equal to or less than the Underwriter’s total lending authority, he/she has the authority to approve the request.

• Example 1 • |

|

Underwriter’s Total Lending Authority |

$75,000 |

Amount Requested and Approved |

$50,000 |

Existing Exposure |

$25,000 |

Total (Potential) Exposure |

$75,000 |

Conclusion: The total potential exposure is equal to or less than the total lending authority of $75,000, so the Underwriter is qualified to give approval. |

|

• Example 2 • |

|

Underwriter’s Total Lending Authority |

$75,000 |

Amount Requested and Approved |

$60,000 |

Existing Exposure |

$25,000 |

Total (Potential) Exposure |

$85,000 |

Conclusion: The total potential exposure is greater than the total lending authority of $75,000, so this Underwriter alone is not qualified to give approval. |

|

Additive and Non-Additive Lending Authority

Your financial institution chose in its setup whether to use additive or non-additive lending authority for Underwriters in a co-decision situation.

Note: The default option is additive lending authority. If you are interested in using the non-additive option, please contact Baker Hill Client Support.

In an additive situation, Baker Hill Origination adds the lending authority amounts for each of the Underwriters, and approval is based on this total sum figure.

In a non-additive situation, the final Underwriter must be able to approve the entire requested loan amount on his or her lending authority alone.

If the Underwriter’s lending limit is insufficient to approve the application, the Underwriter will receive a message saying that the lending authority has not been satisfied and that the application either must be forwarded to another Underwriter for co-decisioning (additive) or must be declined (non-additive).

Please see the following example for further explanation:

• Example • |

|

Underwriter One's Lending Authority |

$50,000 |

Underwriter Two's Lending Authority |

$50,000 |

Amount Requested |

$85,000 |

Additive Lending Authority |

Second Underwriter can approve loan because total combined lending authority of the Underwriters is $100,000. |

Non-Additive Lending Authority |

Second Underwriter cannot approve loan because his/her lending authority is only $50,000; lending authority must be at least $85,000 to approve. |

Co-Decisioning

The specific steps for co-decisioning are described in the Introduction to the Decisioning Process.

For an application to have co-decisioners, all of the following must be met:

The first Underwriter approves and completes the application.

The first Underwriter’s lending limit does not exceed the applicant’s total existing bank exposure.

When prompted about the insufficient lending authority, the first Underwriter selects a co-decisioner.

The second Underwriter (the co-decisioner) completes the application without changing the first Underwriter’s decision in any way. If the second Underwriter changes any aspect of the decision, the first Underwriter will no longer be counted as a decisioner on the application.

Simply forwarding the application to another Underwriter will not count the first Underwriter as a co-decisioner; only the second Underwriter—the one who actually completes the application—will be shown as the decisioner.

An Underwriter can always decline, withdraw, or counter-offer, regardless of lending limits; the lending limit restricts only the Underwriter’s authority to approve.

Score Authority

In setup, your Administrator assigns all users who have been assigned the Underwriter role both a Low Side Score Offset and a High Side Score Offset, based on your financial institution's evaluation cutoff score.

The Low Side Score Offset represents the lower limit of a user's score authority with respect to overriding recommended decisions, and the High Side Score Offset represents the higher limit. For example, suppose your financial institution's evaluation cutoff score is 180, and your score authority range should be 155 to 205. Your Administrator would set your Low Side Score Offset at 25, and the High Side Score Offset at 25. With these settings, if you are overriding the recommended decision on an application with a Total Score of less than or equal to 155 or greater than or equal to 205, the application either must be forwarded to another Underwriter for co-decisioning or must be declined.

When an Underwriter with insufficient score authority chooses to override a recommended decision and attempts to complete the decision, the Lending and/or Score Authority dialog displays. The Underwriter has two options:

Forward the application to another Underwriter with greater score authority by means of this dialog.

Cancel out of the dialog, cancel out of the Decision Application page, and then use the Forward to Another User option on the Home page to send the application to another user (in which case the application will be decisioned completely by the other Underwriter, not co-decisioned by the two Underwriters).

Note: If the co-decisioning path is chosen, note that the last Underwriter in the decision process must meet the score authority required. Score authority is never cumulative, regardless of whether your institution is using additive or non-additive lending authority.